Merry Christmas!!!

The MArS team wishes all a merry and peaceful Christmas and a great start into the New Year!!!

THE German-speaking market access experts - Austria, Germany, Switzerland

The MArS team wishes all a merry and peaceful Christmas and a great start into the New Year!!!

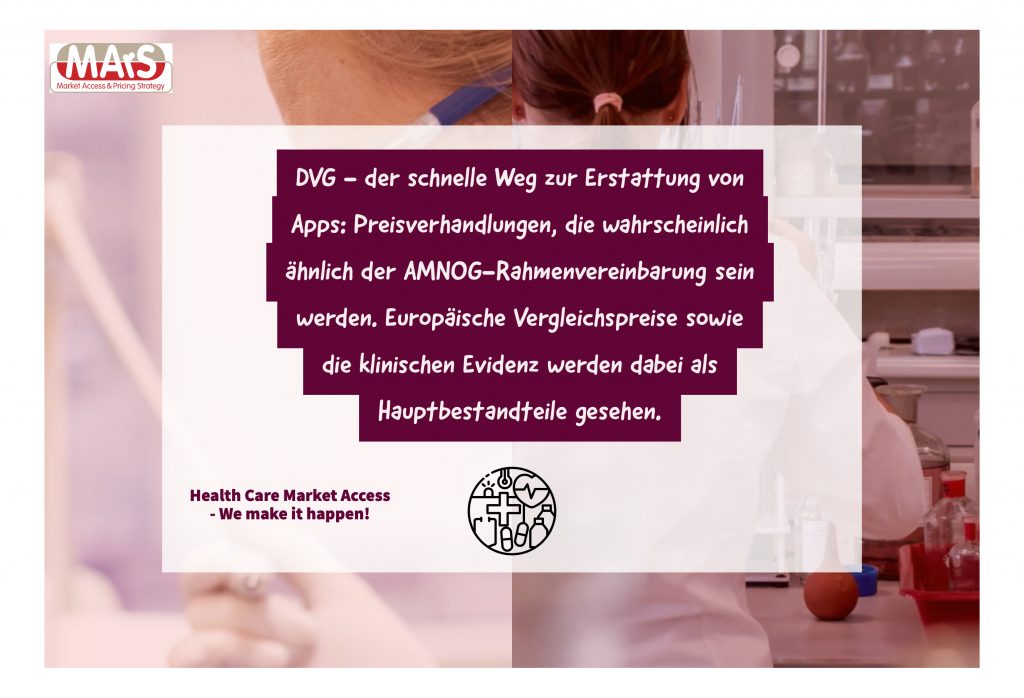

MArS attended the Medical valley Forchheim symposium on the market access pathway for new digital solutions (“apps”) into the statutory health care market. The new law will come into effect January 1 2020. Still open are the templates for the BfArM consultation and the price negotiation frame with the Head association of the statutory health insurance funds (GKV-SV). For the BfArM the regulations can be expected as the new law §33a para. 3 SGB V RefE is now publicly available. In case clinical evidence for a (patient) benefit is proven the app can be included in the BfArM registry / database, if that is not the case this can be provided within the first year of launch.

For the price negotiations MArS expects the regulation frame to be similar (but adapted) as within the AMNOG process. Core drivers will be the European prices (incl.out of pocket cost) as well as the clinical evidence on the product and comparable products. The template for the price negotiations are expected in the next few weeks. The arbitration board is not yet defined and built but is expected soon.

MArS offers the digital industry the experience in the process and contacts with German payers, the BfArM and especially with price negotiations with the GKV-SV. Core services to be provided will be Communication with payers, Pricing – planning, research, design, implementation and Price negotiation.

Sustainability is one of MArS’ core values! Hence MArS has defined four rules of behaviour on which all MArS members work, travel and live.

The availability of Zolgensma in the USA has also fuelled the price discussion for new drugs in Germany. Zolgensma is approved in the USA for the treatment of children with spinal muscular atrophy (SMA) and can (potentially) cure the disease. The drug has not yet been approved in Germany – European approval is expected next year.

Now there are two big discussions in Germany: On the one hand the handling of drugs that have not yet been approved in Germany and on the other hand the pricing of these drugs.

The handling of drugs prior to approval is clearly regulated in the Drug Hardness Ordinance (AMHV) on the so-called Compassionate Use Programme and provides for a cohort programme care of German patients. The drug is made available free of charge! The individual case regulation, which is now also criticized by the health insurance companies, is also clearly regulated by the so-called “Nikolaus” judgment from the year 2005 and is especially made for life-threatening diseases.

As far as the price is concerned, it should be noted that 1) SMA only affects 500 patients throughout Europe, i.e. approx. 80 patients in Germany (!) – so with 100 insurances on average 1 patient per insurance – and 2) without an expectation for high profit in such ultra orphan diseases, no new therapies and medicines will be available in the future either, as the research and investment incentives are then no more given.

Press article on the issue available in German, e.g. in the Badische Zeitung as of November 20 2019: Hoffnung, Leid und viel Geld as well as a comment.

MArS supports you with the optimal reimbursement strategy, pricing for the D-A-CH market and, of course, in a possible early contact and discussion with the statutory health insurance funds.